China surpassed its 2030 renewable energy target of 1,200 GW of combined wind and solar capacity six years ahead of schedule, reaching 1,400 GW by the end of 2024. By the close of 2025, total installed renewable energy capacity exceeded 2,340 GW, accounting for over 60 percent of the country’s total power generation capacity. Renewables now generate nearly 40 percent of China’s electricity.

What Was China’s 2030 Renewable Energy Target?

In 2020, President Xi Jinping announced at the United Nations Climate Ambition Summit that China would install at least 1,200 gigawatts (GW) of combined wind and solar capacity by 2030. This target formed the backbone of China’s nationally determined contribution (NDC) under the Paris Agreement and signaled an aggressive shift toward decarbonization.

At the time, many analysts considered the target ambitious. China had roughly 530 GW of combined wind and solar capacity in 2020, meaning the goal required more than doubling clean energy infrastructure in a single decade. Yet the actual pace of deployment far exceeded every projection.

How China Achieved Its 2030 Goals Six Years Early?

By the end of 2024, China’s combined wind and solar capacity reached approximately 1,400 GW, surpassing the original 1,200 GW target by a wide margin. Solar capacity alone grew by 45.2 percent in 2024, adding 277 GW in a single year. Wind capacity expanded by 18 percent with 80 GW of new installations.

Several policy mechanisms and market forces drove this acceleration. Government-backed feed-in tariffs during the early years created initial momentum. As manufacturing costs plummeted through economies of scale, new mechanisms such as green electricity certificates and competitive auctions sustained the build-out. China’s domestic solar manufacturing capacity alone reached 1,200 GW per year by late 2025, exceeding total global annual demand.

Key Milestones in China’s Renewable Energy Timeline

| Year | Milestone |

| 2020 | Xi Jinping announces 1,200 GW wind and solar target for 2030 |

| 2023 | China adds 217 GW solar and 76 GW wind; total reaches 1,050 GW |

| 2024 | Combined capacity hits 1,400 GW, surpassing 2030 target six years early |

| Mid-2025 | Wind and solar capacity overtakes coal for the first time in installed capacity |

| End of 2025 | Total renewable capacity exceeds 2,340 GW; renewables account for 60 percent of installed power |

Current Status: China’s Renewable Energy Capacity

China added more than 430 GW of new wind and solar capacity during 2025, bringing total wind and solar capacity above 1,800 GW. When including hydropower, biomass, and other renewable sources, total installed renewable capacity reached approximately 2,340 GW by year-end, representing over 60 percent of the nation’s total power generation capacity of 3.89 terawatts.

Renewable electricity generation reached approximately 4 trillion kilowatt-hours during 2025, a figure that exceeds the combined annual power consumption of all 27 European Union member states. China also became the first country in the world to surpass 1,000 GW of installed solar capacity, hitting this milestone during the first half of 2025. By year-end, solar capacity alone reached an estimated 1,200 GW, while wind stood at approximately 640 GW.

Capacity Breakdown by Source (End of 2025)

| Energy Source | Installed Capacity (GW) | Share of Total Renewables |

| Solar PV | ~1,200 | ~51% |

| Wind (Onshore and Offshore) | ~640 | ~27% |

| Hydropower | ~442 | ~19% |

| Biomass and Others | ~58 | ~3% |

| Total Renewables | ~2,340 | 100% |

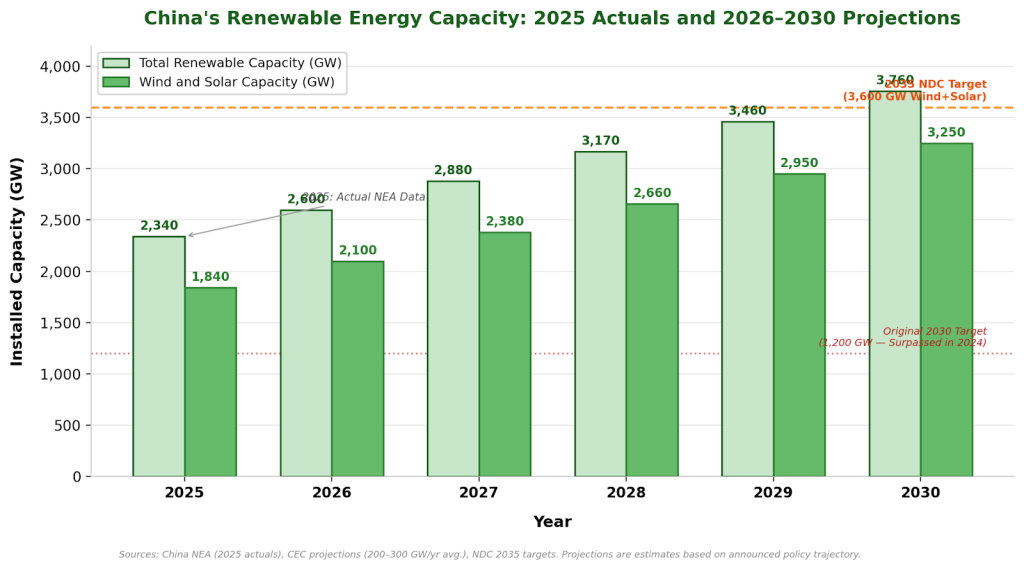

Projected Growth: 2025 to 2030 Capacity Outlook

The China Electricity Council projects average annual new renewable capacity additions of 200 to 300 GW during the 15th Five-Year Plan period (2026 through 2030). Based on this trajectory, China’s total renewable energy capacity could approach 3,800 GW by 2030, with wind and solar alone potentially reaching 3,250 GW. This would put the country well on track toward its 2035 NDC target of 3,600 GW of wind and solar capacity.

Figure 1: China Renewable Energy Capacity – 2025 Actuals and 2026–2030 Projections (GW)

As illustrated above, China’s wind and solar additions are expected to add roughly 250 to 300 GW annually, driven by continued government support, falling technology costs, and expanding grid infrastructure. The original 2030 target of 1,200 GW, shown at the bottom of the chart, underscores how dramatically China has outperformed its own goals. The 2035 NDC target of 3,600 GW for wind and solar appears increasingly achievable well before the deadline.

Record Investment Fueling the Transition

Unprecedented capital flows support China’s clean energy build-out. In 2024, the country attracted $625 billion in clean energy investment, representing 31 percent of the global total of $2,033 billion. Total energy project investment topped 3.5 trillion yuan (approximately $500 billion) in 2025, an 11 percent year-over-year increase and a record for any single country in a single year.

Battery storage deployment has emerged as a critical enabler of this transition. The volume of installed battery storage tripled in the three years leading up to 2024, and newly installed energy storage capacity exceeded 100 GW during 2025, accounting for over 40 percent of global capacity. Investment in battery storage rose 69 percent between the first halves of 2024 and 2025, while grid investment increased 22 percent during the same period.

This massive deployment is reshaping global clean energy economics. As Chinese manufacturers have scaled production, the costs of solar panels, wind turbines, and batteries have fallen dramatically. These cost reductions affect pricing across international markets, influencing everything from EV price floors in the EU and the US to the broader cost structure of decarbonization worldwide.

China’s Renewable Energy Policy Framework

China’s renewable energy strategy operates through a multi-layered policy architecture. The “1+N” framework issued in 2021 establishes the overarching goal of peaking carbon emissions before 2030 and achieving carbon neutrality by 2060. Under this umbrella, specific Five-Year Plans, sectoral action plans, and provincial deployment targets translate national ambitions into on-the-ground installations.

Key Policy Drivers

- 14th Five-Year Plan (2021-2025): Set a target for renewables to supply 33 percent of electricity by 2025 and total installed capacity to reach 3,000 GW across all sources.

- Green Electricity Certificate Trading: Expanded dramatically during 2025, providing additional revenue streams for renewable energy developers and incentivizing deployment.

- Unified National Electricity Market: Creation of a single power trading market to facilitate renewable energy integration and ensure low-cost clean power reaches consumers across the country.

- Desert-Based Mega-Projects: Large-scale wind and solar installations in China’s western desert regions, connected to population centers through ultra-high-voltage transmission lines.

Looking Ahead: The 2035 NDC Targets

In November 2025, China submitted its updated nationally determined contribution with new targets for 2035. The key commitments include expanding wind and solar capacity to 3,600 GW (six times the 2020 level), raising the share of non-fossil fuels in total energy consumption above 30 percent, and reducing economy-wide net greenhouse gas emissions by 7 to 10 percent from peak levels.

While some analysts consider these targets conservative given the current pace of deployment, China has a well-documented pattern of setting achievable goals and exceeding them. The Centre for Research on Energy and Clean Air estimates that clean energy industries could double in value by 2035, adding approximately 15 trillion yuan ($2.1 trillion) to China’s economy. This economic dimension is critical, as green technologies already accounted for up to 10 percent of China’s GDP in 2024.

The acceleration of robotics and AI-driven automation in clean energy manufacturing is also expected to reduce deployment costs further. Companies across the emerging robotics sector, including firms like Unitree and Kepler, are developing solutions that could streamline production lines for solar panels, battery systems, and wind turbine components.

Global Impact and Supply Chain Dominance

China’s renewable energy expansion has far-reaching global implications. The country manufactures over 80 percent of the world’s solar panels, around 60 percent of wind turbines, and 75 percent of electric vehicles and their batteries. Chinese companies now account for approximately 75 percent of global clean energy patent applications, up from just 5 percent in 2000.

This supply chain dominance creates both opportunities and tensions. On one hand, cheap Chinese manufacturing has enabled 25 percent of emerging markets to leapfrog the US in end-use electrification, according to Ember’s analysis. On the other hand, trade frictions over subsidies, tariffs, and industrial policy are intensifying. The pricing of imported green technologies has become a significant factor in consumer markets globally, affecting costs that ultimately flow through to household budgets. The ripple effects on tariff-driven pricing changes across consumer goods illustrate how interconnected these dynamics have become.

Remaining Challenges

Despite the scale of its achievements, China faces real obstacles in its energy transition:

- Coal dependency persists: Coal still accounted for 58 percent of power generation in 2024, and China continues to approve new coal-fired plants, raising concerns about carbon lock-in.

- Grid integration bottlenecks: Average power plant utilization fell by 312 hours in 2025, indicating that capacity is growing faster than grid flexibility and transmission infrastructure can accommodate.

- Curtailment risk: Without adequate storage and transmission, significant amounts of wind and solar generation may be wasted, particularly in western provinces far from major demand centers.

- Carbon intensity targets: China risks falling short of its CO2 emissions intensity reduction targets under the 14th Five-Year Plan, partly due to slower economic growth and post-pandemic effects.

What does this mean for the Global Energy Transition?

The International Energy Agency has identified China’s progress as critical to keeping the global goal of tripling renewable capacity by 2030 within reach. In 2024, China accounted for more than half of the global increase in renewable energy capacity. The Climate Action Tracker projects that 2025 may mark the peak of China’s CO2 emissions, with clean energy growth contributing to a 1 percent year-over-year decline in CO2 emissions during the first half of the year.

China’s 15th Five-Year Plan, expected to be formalized in early 2026, will further define deployment targets for 2026 through 2030. The China Electricity Council anticipates average annual new installed renewable capacity of 200 to 300 GW during this period, maintaining the current pace of expansion.

For the rest of the world, the message is clear: large-scale energy transformation is technically feasible and economically viable when supported by sustained policy commitment and industrial capacity. Whether other nations can replicate this speed depends on their own policy environments, grid infrastructure, and willingness to invest at comparable scales.